Unlock Your Retirement: From Workplace Burnout to Financial Freedom

Feeling worn out at work and thinking about retirement? Wondering if your super will be enough and how you’ll manage your income when you stop working? In this episode, Rob…

Feeling worn out at work and thinking about retirement? Wondering if your super will be enough and how you’ll manage your income when you stop working? In this episode, Rob…

The average Australian is sitting on a balance of 73,000 frequent flyer points, according to a 2025 survey. About a quarter of those surveyed used their points for travel occasionally,…

Feeling overwhelmed by HECS debt and the dream of owning a home? Rob Goudie and Ash Rowan tackle this crucial financial question. Ash shares his personal journey of clearing HECS…

What’s the first thing that springs to mind when you hear the term ‘passive income’? It may be creating an e-book, a blog or a YouTube channel, engaging in affiliate…

When life throws you a curveball and you suddenly can’t work, the financial pressure can feel overwhelming. But here’s something many Australians don’t realise: there can be many safety nets…

What really happens to your Age Pension, Centrelink benefits, and aged care fees when one partner passes away? Rob Goudie and Ash Rowan explore a real-life case study revealing one…

The December quarter has been defined by unexpected twists. Just as we thought inflation was under control, it kicked back up. Just as rate cuts seemed certain for 2026, we’re…

There’s a growing issue facing families today, and it spans three generations. At the heart of it is the younger generation—the first-time homebuyers—who are struggling to break into the property market. This challenge isn’t just theirs to bear; it’s one that also involves their parents and grandparents, who want to see them succeed but are grappling with how to provide the right kind of support without overstepping or creating dependency.

Scams are everywhere—and they’re getting smarter. In this episode, Rob Goudie is joined by Rachel Todman to discuss the growing threat of scams, especially during the Christmas period when urgency…

Thinking about setting up a Self-Managed Super Fund? Before you do, this episode could save you years of costly mistakes. In this episode, Amy Lehmann and Rob Goudie break down…

In this episode , Rob Goudie is joined by long-term advisor and partner Ash to discuss real-world aged care case studies and the financial decisions that impact families. They unpack…

There’s a growing issue facing families today, and it spans three generations. At the heart of it is the younger generation—the first-time homebuyers—who are struggling to break into the property market. This challenge isn’t just theirs to bear; it’s one that also involves their parents and grandparents, who want to see them succeed but are grappling with how to provide the right kind of support without overstepping or creating dependency.

In today’s episode, Rob is joined by business partner Ashley, an expert in aged care and retirement planning. Together, they break down the major changes to aged care and home…

From early November retailers have been telling us what we can’t live without and what our kids must have if they are to still love us on Christmas Day. It’s easy to get caught up in the momentum. Of course, the downside is you end up with the post-Christmas blues when the credit card statements arrive. This may mean that wealth plans get scrapped because you have to pay off the debt first.

As you progress towards retirement age, the idea of reducing your working hours can be appealing, especially if you can do it without reducing your income. Fortunately, there is a way to do this. It’s called a Transition to Retirement Income Stream (TTRIS), which allows you to supplement your part-time income with regular payments from your superannuation savings.

Thinking about selling your business or farm? Before you make the leap, make sure you’re not walking away from opportunities or walking into avoidable mistakes. Rob and Amy break down…

Aged care is about to become far more expensive, and most families have no idea what’s coming. In this episode of the Investor Motivation Podcast, Rob and Ash unpack the…

In this episode, Amy and Rob break down the newly updated superannuation tax changes and what they mean for investors. They discuss the revised $3 million and $10 million thresholds,…

Ever wondered why no matter how much you earn, money still feels stressful sometimes? It’s not just numbers, it’s emotions, habits, and mindset at play. In this episode, we dive…

In this episode, Robert Goudie and Amy Lehmann breaks down everything you need to know about mortgages, from why managing your loan with care is crucial, to real cash flow…

Ever Googled questions like “Can investing make you rich?” or “Is investing better than saving?” You’re not alone! In this episode of the Investor Motivation Podcast, Amy Lehmann and Robert…

Despite the temporary, sudden downturns caused by the 2007-2009 global financial crisis and the 2020-2021 COVID pandemic, the value of the ASX increased by more than 160% between 2000 and 2024, as evidenced by the growth in the ASX 200 market index. This demonstrates that it’s better to invest in a variety of shares rather than sticking to just a few.

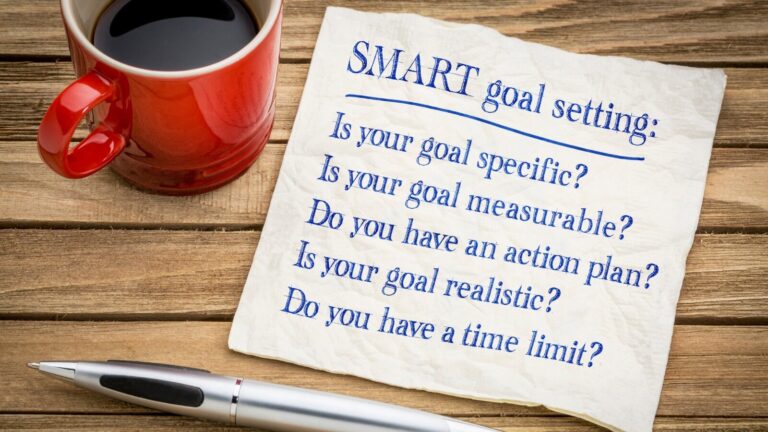

In the context of your personal finances, SMART refers to setting clear, quantifiable, feasible and appropriate financial objectives, to be carried out within a defined time frame. You’re much more likely to succeed if you avoid vague, non-measurable, unrealistic and inappropriate aims with no actual deadline. Relying on SMART goals will help you stay on track as you shape your financial future.

The opinion of many people towards debt can be best summed up in the often quoted line from Shakespeare, ‘neither a borrower nor a lender be.’ Yet others will embrace…

End of content

End of content