Blended families and money: How to protect assets fairly

About one in 10 families in Australia is a blended or step family, according to census data, and this trend has increased in recent years. Blended families can work well,…

About one in 10 families in Australia is a blended or step family, according to census data, and this trend has increased in recent years. Blended families can work well,…

The 2026 Federal Budget has introduced some of the most significant proposed tax changes Australia has seen in years. While many of the announcements were expected following months of speculation…

Home ownership – is it still the Great Australian Dream? According to a recent survey, it is, but the option of renting for life is becoming increasingly attractive.

The average Australian is sitting on a balance of 73,000 frequent flyer points, according to a 2025 survey. About a quarter of those surveyed used their points for travel occasionally,…

When most people think about financial advice, they picture investments, superannuation, or maybe insurance. But the true value of advice isn’t just about the numbers, it’s about what those numbers allow you to do in your life.

When most people think about financial advice, they picture investments, superannuation, or maybe insurance. But the true value of advice isn’t just about the numbers, it’s about what those numbers allow you to do in your life.

When life throws you a curveball and you suddenly can’t work, the financial pressure can feel overwhelming. But here’s something many Australians don’t realise: there can be many safety nets…

Talking to children about money can sometimes feel awkward, but the truth is they are learning from us every day. The way we spend, save, and talk about money shapes their attitudes well into adulthood. By teaching kids healthy money habits early, we give them confidence and skills that will last a lifetime.

When we think about health, we often picture diet, exercise, or regular check-ups. What we do not always think about is money. Yet financial wellbeing and overall wellbeing are closely linked.

When it comes to money, more is not always better. Multiple super funds, a handful of bank accounts, different investment platforms, and stacks of paperwork can make it hard to see the bigger picture. Simplifying your finances can reduce stress and often leads to better results.

It is natural to want to enjoy the rewards of hard work. A new job, a pay rise, or a bonus can make it tempting to upgrade your car, move to a bigger house, or start spending more on dining and holidays. This is called lifestyle creep, and while it feels good in the short term, it can quietly slow down your long-term financial goals.

If you’ve ever dreamed of setting up your own business you’re not alone.

According to the Australian Bureau of Statistics, (ABS), in the financial year 2023 – 2024 over 400,000 Aussies did just that!

Over the same period, almost 363,000 small businesses called it quits.

Despite a slowdown in Australian economic and productivity growth in the last five years, Australia’s economy is usually considered strong and resilient when compared with other developed nations. Given our economic strength, why would anyone want to invest anywhere else?

To answer this question, let’s consider what stocks might be included in a share portfolio with an international focus.

For simplicity purposes, we will look into the portfolios of a leading provider of index managed funds and their top 10 holdings. These funds tend to be passively rather than actively traded, and seek to reflect their chosen share index over the medium-to-long term.

A client once shared a poignant regret:

“When I was working and the kids were young, I saved too much. It restricted what we did when the family was together.”

This simple reflection struck a chord with me. It got me thinking about the delicate balance between saving for the future and living fully in the present. While we all know the importance of financial security, is it possible to save too much—at the expense of the moments that matter most?

Buying a home in Australia has become a monumental challenge. With skyrocketing property prices and average mortgage debts exceeding $600,000, many young Australians feel homeownership is out of reach. As…

A client once shared a poignant regret:

“When I was working and the kids were young, I saved too much. It restricted what we did when the family was together.”

This simple reflection struck a chord with me. It got me thinking about the delicate balance between saving for the future and living fully in the present. While we all know the importance of financial security, is it possible to save too much—at the expense of the moments that matter most?

Remember that old ad with the guy proudly polishing his boat while his neighbor asks, “How do you afford all this?” His response—“Equity, mate”—has stuck in the Australian psyche for…

A client once shared a poignant regret:

“When I was working and the kids were young, I saved too much. It restricted what we did when the family was together.”

This simple reflection struck a chord with me. It got me thinking about the delicate balance between saving for the future and living fully in the present. While we all know the importance of financial security, is it possible to save too much—at the expense of the moments that matter most?

Why Traditional Budgeting Fails We’ve all been told that the key to managing money is to create a budget and stick to it. Track every dollar, set spending limits, and…

As a financial adviser, one of the most common discussions I have with clients is about helping their children financially. For those with the means, the question isn’t if they…

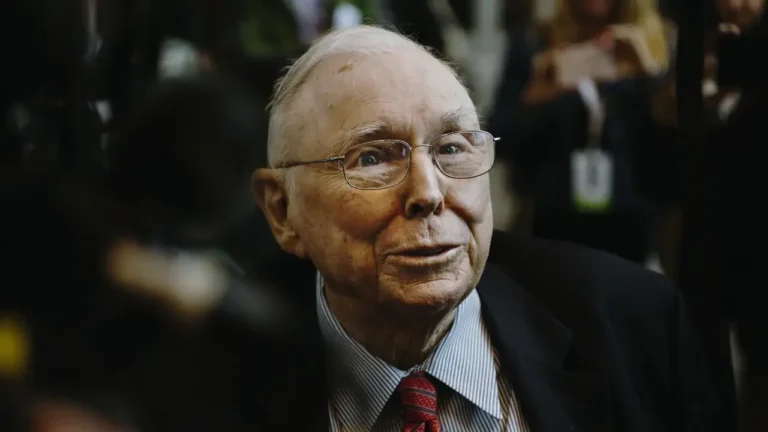

As a financial adviser, I often find inspiration in the words of seasoned investors who have spent decades mastering their craft. While Warren Buffett tends to grab the spotlight, his…

Share markets are renowned for taking unexpected downturns and while history shows that markets eventually recover, this rebound in value can occasionally take time. Investors concerned about this risk might…

The days leading to Christmas, holidays and celebrations are exciting, frenetic times. They’re a whirl of parties and social engagements, gifts and food to be purchased and travel arranged. The…

Struggling to keep track of multiple debt payments each month? For many Australian homeowners, juggling different debts—whether it’s credit card balances, personal loans, or mortgage repayments—can become overwhelming. Debt consolidation…

End of content

End of content