Loyalty tax – are you paying more than you should?

Sandy joined her local gym a decade ago. She was proud of her long-member status and was content to pay the monthly $200 fee.

Sandy joined her local gym a decade ago. She was proud of her long-member status and was content to pay the monthly $200 fee.

Everywhere you look, property investment is being marketed like a golden ticket to wealth. Social media is flooded with experts explaining how to structure loans, access equity, and leverage your superannuation to get into the property market.

When we think about health, we often picture diet, exercise, or regular check-ups. What we do not always think about is money. Yet financial wellbeing and overall wellbeing are closely linked.

You may be one of many Australians who make an interest-free loan to the federal government every year. That’s because, when you receive a tax refund, you’re not getting free money. All that’s happening is that cash which is rightfully yours is being returned, somewhat late. So it makes sense to make it work as hard as possible once it’s back in your hands.

When it comes to investing, most of us focus on what to invest in—shares, property, or superannuation. But there’s another decision that’s just as important: where you hold those investments….

When clients ask, “Do I have enough to last through retirement?”, it’s often one of the biggest and most emotional questions they face. After nearly 27 years as a financial…

Over the last 20 years, I’ve shaped my investment philosophy and business around one central idea: direct investing. Rather than relying heavily on managed funds or exchange-traded funds (ETFs), I…

Buying a home in Australia has become a monumental challenge. With skyrocketing property prices and average mortgage debts exceeding $600,000, many young Australians feel homeownership is out of reach. As…

Australians love a good tax deduction. It’s almost ingrained in us—if there’s a way to pay less tax, we’re all ears. But what happens when tax savings become the main…

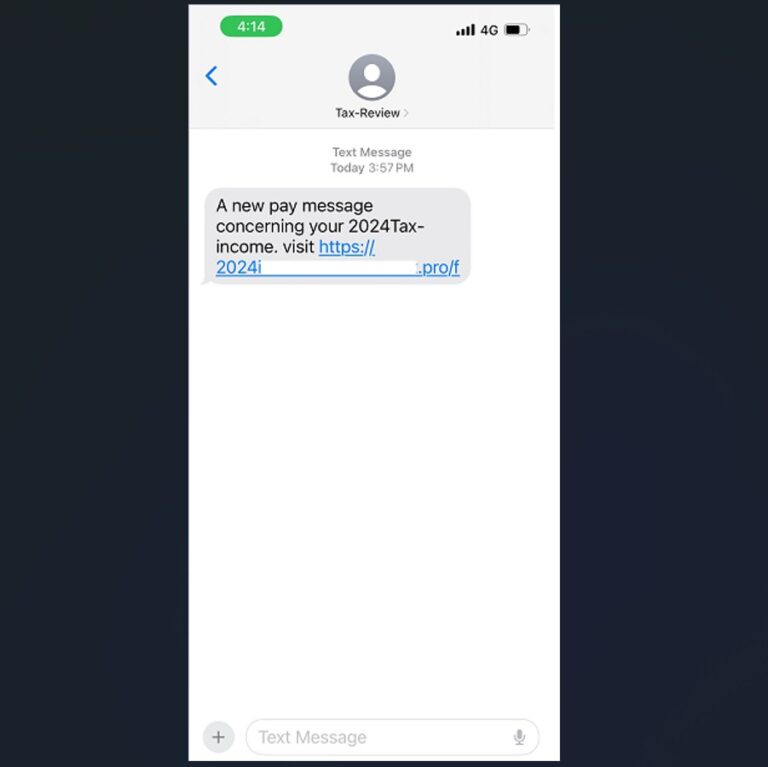

CPA Australia Australians should always be wary of online scams, but we are particularly vulnerable at tax time. Cyber criminals use a mix of tried-and-tested and new methods to attempt…

CPA Australia No one likes being treated as just a number, but with millions of returns and tens of billions of dollars at stake, that’s the reality when it comes…

Looking to give your super a boost before the end of the financial year? Look no further! Follow these five strategies to maximise your contributions and make the most of…

Australian Taxation Office As ‘tax time’ approaches, the Australian Taxation Office (ATO) has announced it will be taking a close look at 3 common errors being made by taxpayers: •…

In his 2024 Federal Budget speech, treasurer, Jim Chalmers, announced that ‘The number one priority of this government and this Budget is helping Australians with the cost of living’. But…

When it comes to getting the most (money) from your annual tax return, there is usually a lot to think about, so we’ve identified a few options that could open…

When you’re at the helm of your own business, it’s easy to get caught up in the whirlwind of the present – chasing sales, generating leads, and growing your business….

Lady Luck has once again looked down fondly upon Australia, creating the first Federal Budget surplus in 15 years, through a higher tax take on record export earnings and increasing…

If you’re a freelancer or contractor or maybe even a consultant then you’re part of the “gig economy”. Gone is the job for life, or even a job in the…

Here is a list of tips to help you minimise the amount of tax you pay this end of financial year: 1. Keep records Even if you use an accountant…

As the end of financial year fast approaches, there is still time to consider the strategies available to you this June 30 to build your wealth, some of which are…

The end of another financial year is looming, and with that may come thoughts about your tax return and how your wealth has tracked throughout the year. Whether you’re nearing…

With the range of technology and software available today, it’s become easier than ever to work from home. Employees can efficiently complete calls using teleconferencing software, many collaboration tools are…

Thousands of Australians receive tax refunds every year. Some refunds won’t even cover the cost of a pizza to celebrate, however many are quite substantial. If you’re one of the…

End of content

End of content