Loyalty tax – are you paying more than you should?

Sandy joined her local gym a decade ago. She was proud of her long-member status and was content to pay the monthly $200 fee.

Sandy joined her local gym a decade ago. She was proud of her long-member status and was content to pay the monthly $200 fee.

Some of the most meaningful work I do as a financial adviser happens during the hardest seasons of a person’s life.

Losing a partner is one of those moments.

When most people think about financial advice, they picture investments, superannuation, or maybe insurance. But the true value of advice isn’t just about the numbers, it’s about what those numbers allow you to do in your life.

When most people think about financial advice, they picture investments, superannuation, or maybe insurance. But the true value of advice isn’t just about the numbers, it’s about what those numbers allow you to do in your life.

When life throws you a curveball and you suddenly can’t work, the financial pressure can feel overwhelming. But here’s something many Australians don’t realise: there can be many safety nets…

We all have a “money story.” It is the set of beliefs, habits, and emotions we carry about money, often shaped long before we ever earned our first paycheck. We all have a “money story.” It is the set of beliefs, habits, and emotions we carry about money, often shaped long before we ever earned our first paycheck.

There’s a growing issue facing families today, and it spans three generations. At the heart of it is the younger generation—the first-time homebuyers—who are struggling to break into the property market. This challenge isn’t just theirs to bear; it’s one that also involves their parents and grandparents, who want to see them succeed but are grappling with how to provide the right kind of support without overstepping or creating dependency.

There’s a growing issue facing families today, and it spans three generations. At the heart of it is the younger generation—the first-time homebuyers—who are struggling to break into the property market. This challenge isn’t just theirs to bear; it’s one that also involves their parents and grandparents, who want to see them succeed but are grappling with how to provide the right kind of support without overstepping or creating dependency.

Money is one of the most common sources of stress in relationships. Whether it is with a partner, family member, or even a business partner, the way we think about and manage money can have a big impact on how we relate to each other.

Many Australians find themselves in what is called the “sandwich generation.” This is the stage of life where you may still be supporting children while also stepping in to care for ageing parents. It can feel like you are being pulled in two directions, both emotionally and financially.

Life does not always go to plan. Illness, job loss, accidents, or unexpected expenses can arrive without warning. While we cannot prevent these events, we can prepare for them. Having the right protections in place provides peace of mind and ensures your family is supported when life takes a turn.

There’s no shortage of financial advice out there. Everywhere you look—social media, news articles, investment forums—you’re bombarded with strategies, opinions, and predictions.

Despite the temporary, sudden downturns caused by the 2007-2009 global financial crisis and the 2020-2021 COVID pandemic, the value of the ASX increased by more than 160% between 2000 and 2024, as evidenced by the growth in the ASX 200 market index. This demonstrates that it’s better to invest in a variety of shares rather than sticking to just a few.

When it comes to money, it is often the small, consistent steps that make the biggest difference. You do not need to make dramatic changes overnight. Building good habits and sticking with them over time can transform your financial future.

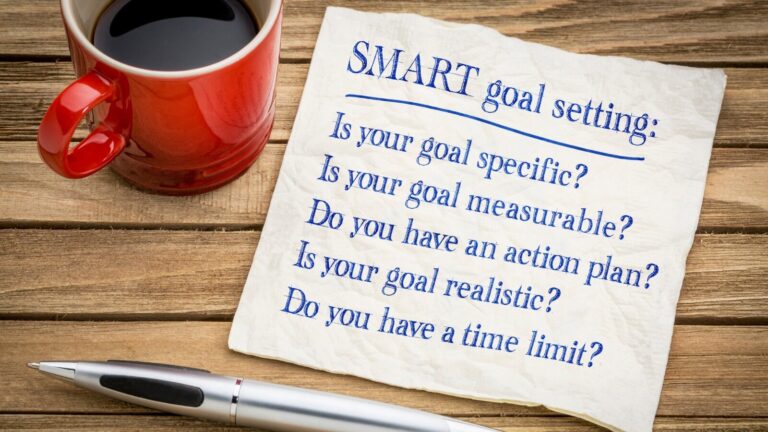

In the context of your personal finances, SMART refers to setting clear, quantifiable, feasible and appropriate financial objectives, to be carried out within a defined time frame. You’re much more likely to succeed if you avoid vague, non-measurable, unrealistic and inappropriate aims with no actual deadline. Relying on SMART goals will help you stay on track as you shape your financial future.

Over the last few years, I’ve taken on the management of many self-managed superannuation funds (SMSFs), and in doing so, I’ve encountered a particular investment type that often causes significant…

When we think about health, we often picture diet, exercise, or regular check-ups. What we do not always think about is money. Yet financial wellbeing and overall wellbeing are closely linked.

The opinion of many people towards debt can be best summed up in the often quoted line from Shakespeare, ‘neither a borrower nor a lender be.’ Yet others will embrace…

It is natural to want to enjoy the rewards of hard work. A new job, a pay rise, or a bonus can make it tempting to upgrade your car, move to a bigger house, or start spending more on dining and holidays. This is called lifestyle creep, and while it feels good in the short term, it can quietly slow down your long-term financial goals.

You may be one of many Australians who make an interest-free loan to the federal government every year. That’s because, when you receive a tax refund, you’re not getting free money. All that’s happening is that cash which is rightfully yours is being returned, somewhat late. So it makes sense to make it work as hard as possible once it’s back in your hands.

If you’ve ever clicked on a Facebook or Instagram ad about paying off your home loan in under 10 years, chances are you’ve been bombarded with more of them since. I’m all for reducing debt as quickly as possible. But let’s be real: not all strategies are created equal, and not all of them are safe.

When you have a spare $500 and are wondering whether to spend it or save it, why not consider a third option?

Invest it. Make a commitment to your financial future, instead of wasting it on purchases that will deliver only temporary pleasure.

Invest that $500 and watch it grow. Here’s how.

When it comes to investing, most people focus on picking the right stocks, finding the best superannuation fund, or minimising their tax bill. And don’t get me wrong, these things…

Despite a slowdown in Australian economic and productivity growth in the last five years, Australia’s economy is usually considered strong and resilient when compared with other developed nations. Given our economic strength, why would anyone want to invest anywhere else?

To answer this question, let’s consider what stocks might be included in a share portfolio with an international focus.

For simplicity purposes, we will look into the portfolios of a leading provider of index managed funds and their top 10 holdings. These funds tend to be passively rather than actively traded, and seek to reflect their chosen share index over the medium-to-long term.

End of content

End of content