Setting SMART financial goals that actually stick

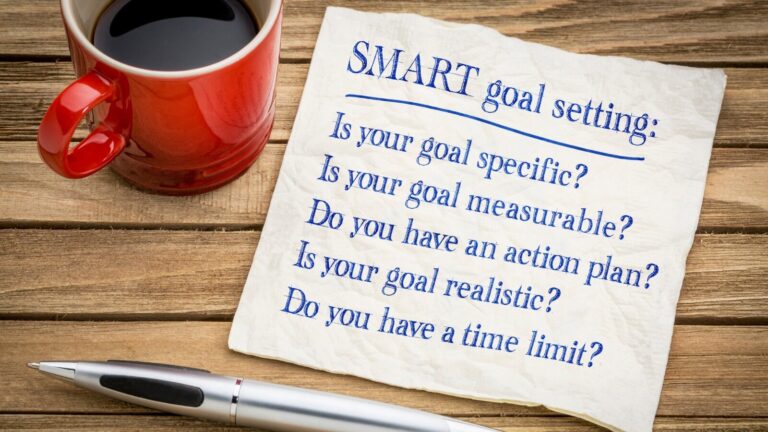

In the context of your personal finances, SMART refers to setting clear, quantifiable, feasible and appropriate financial objectives, to be carried out within a defined time frame. You’re much more likely to succeed if you avoid vague, non-measurable, unrealistic and inappropriate aims with no actual deadline. Relying on SMART goals will help you stay on track as you shape your financial future.